The Content is for informational purposes only, you should not construe any such information or other material as legal, tax, investment, financial, or other advice. Investing involves risk, please consult a financial professional before making an investment.

Robinhood is a zero-commission brokerage that was founded in 2013. It has a beautiful mobile user interface that game-ifies the gambling of your life savi—, er, makes it seamless for millennials to buy and sell stocks.

I wrote on Quora in Dec 2014 on why lowering the barrier to entry to this extent can cause retail investors to make trades without knowing what they are doing. That post turned out to be rather prescient, for reasons I’ll explain below.

One of the ways Robinhood makes money is via margin lending: they loan you some extra money to invest in the stock market with, and later you pay back the loan with some interest (currently about 5%).

If you are in the business of lending money, not only do you have to safeguard your brokerage system against technological vulnerabilities (e.g. C++ memory leaks that expose users’ trades), but you also need to defend against financial vulnerabilities, which are portfolios that expose the lender or its customers to an irresponsible amount of investment risk.

In the last few months it has come to light [1, 2, 3, 4, 5] that there are some serious financial vulnerabilities in Robinhood’s margin lending platform, whereby it is possible for users to borrow much, much more money from Robinhood than they are supposed to.

These users subsequently gamble huge amounts of borrowed money away in a coin toss, leaving Robinhood in a very bad spot, perhaps even at odds with Regulation T laws (I am not a lawyer, just speculating here).

“Leverage” is one of the most important concepts to understand in finance, and when used judiciously, is a net positive for everyone involved. It is important for everyone to understand how credit works, and how much leverage is too much. Borrowing more money than you can afford to pay back can take many forms, whether it is taking on college debt, credit card debt, or raising VC money.

Here’s a tutorial on “financial leverage” in the form of a story about lemonade:

It’s a hot summer, and you decide to start a lemonade stand to make some money. You have 100€, with which you can buy enough ingredients to make 120€ of lemonade for the summer. Your “return on investment”, or ROI, for the summer is 20%, since you ended up with 20% more money than you started with.

You also figure that if you had another 200€, enough people want lemonade that you could sell three times as much lemonade and make 360€. But you don’t have 200€ to spare! What do you do?

You could use the 120€ to build a slightly bigger lemonade operation next year. Assuming you could get a 20% ROI again next summer, you end up with 144€. But it will be many years before you even have 300€! By this time next year, lemonade might be out of fashion and kids might be juuling at home watching Netflix instead. You would much prefer to scale up your lemonade operation now, while you are confident that you can sell lemonade at a "profit margin" of 20%.

Fortunately, your friend “Britney Banker” is very wealthy and can lend you 200€. Britney Banker doesn’t have your entrepreneurial spirit, so she lacks the ability to get a 20% ROI on her own money. She offers to give you 200€ today, in exchange for you giving her 210€ at the end of the year -- an interest rate of 5%. Your “capital leverage ratio” is 100 / 200 = 1:2, because for every dollar you own, Britney is willing to lend you 2€.

If things turn out well, you sell 360€ worth of lemonade, pay Britney back 210€, and pocket the remaining 150€. Starting with 100€, you were able to use borrowed money to “magnify” your return to 50%.

However, if you make 200€ worth of lemonade and fail to sell any of it before the lemonade spoils and became worthless, you would be in a very sticky situation! You would have worthless lemonade and a 210€ debt to Britney. This is far worse than if you had lost your own 100€, because at least you wouldn’t owe anyone anything afterwards. So even though 1:2 leverage may amplify your gains from 20% → 50%, so it may amplify your potential losses from 100% → -310%!

The only reason why Britney is willing to lend you the money in the first place is that Britney thinks this outcome (you losing all of the borrowed money on top of your own assets) is unlikely. If Britney thought that you were less reliable, she might offer you a smaller leverage ratio (e.g. 1 : 1.5).

Suppose you make a big batch of lemonade (with Britney’s money) and then go door to door selling lemonade, but instead of giving customers a delicious drink right away, you give them a “deep-in-the-lemonade covered call option”. You take their money up front, and give them a coupon that allows them to “buy” a lemonade for free (0€).

The "call option" is referred to as "covered" because you actually have the lemonade to go with the coupon, it's just that you're holding onto the lemonade until the buyer actually redeems the coupon.

You then go back to Britney and say “I have 360€ of lemonade that I’ve made but haven’t sold, and 360€ in cash from selling lemonade options to customers, and as for debts there’s 200€ I’ve borrowed from you. That’s 520€ in net assets, so can I please borrow 1040€?”.

Britney says “sure, that’s a 1:2 leverage ratio”, and writes you a check for 1040€, again with 5% interest. But Britney has made a tragic mistake here! The 360€ in lemonade she counted as your assets are not really yours to spend, because you actually owe them in obligations to customers.

With 1204€ in borrowed assets, you are now leveraged over 1:12 !

You repeat this process again, turning 1040€ cash into 1248€ of lemonade, selling an additional 1248€ of deep-in-the-lemonade options. You now have 1608€ of lemonade, and 1608€ in cash, and 1204€ of debt, for net assets of 1608 + 1608 - 1204 = 2012€.

You go back to Britney and ask to borrow another 4024€, with 5% interest. Again, because Britney is forgetting to account for the 1608€ in lemonade “debt” that you may have to deliver to coupon-holders, she thinks that the leverage is still 1:2. You repeat this process one more time, and your new total position is 6k€ in lemonade, 6k€ in cash, 5k€ net debt.

If you were to successfully deliver 6k€ of lemonade, you would make 1k€ in profit, starting from only 100€ of your own cash. A 1000% return sounds too good to be true, right? That’s because it is.

One hot summer day, all of the coupon holders decide to exercise their coupons at the same time. You realize that your lemonade stand can’t actually fulfill 6k€ in lemonade orders and you are in way over your head. Desperate, you attempt to pivot and come up with a Billy Mcfarland-esque scheme to buy lemonade from a local grocery and dilute it with some water. But due to inexperience with food handling operations, you accidentally contaminate half the batch, and are left with only 3k€ of lemonade. You have 6k€ cash but still owe 3k€ in lemonade and 5k€ in cash.Your 1k€ profit opportunity has now become a 2k€ DEBT (ROI of -2100%), and we haven't even factored in the interest! Because the debtors (lemonade coupon holders and Britney Banker) must be paid regardless of whether you successfully make lemonade or not, your leverage has an asymmetric payoff - the downsides are twice as bad as the upside!

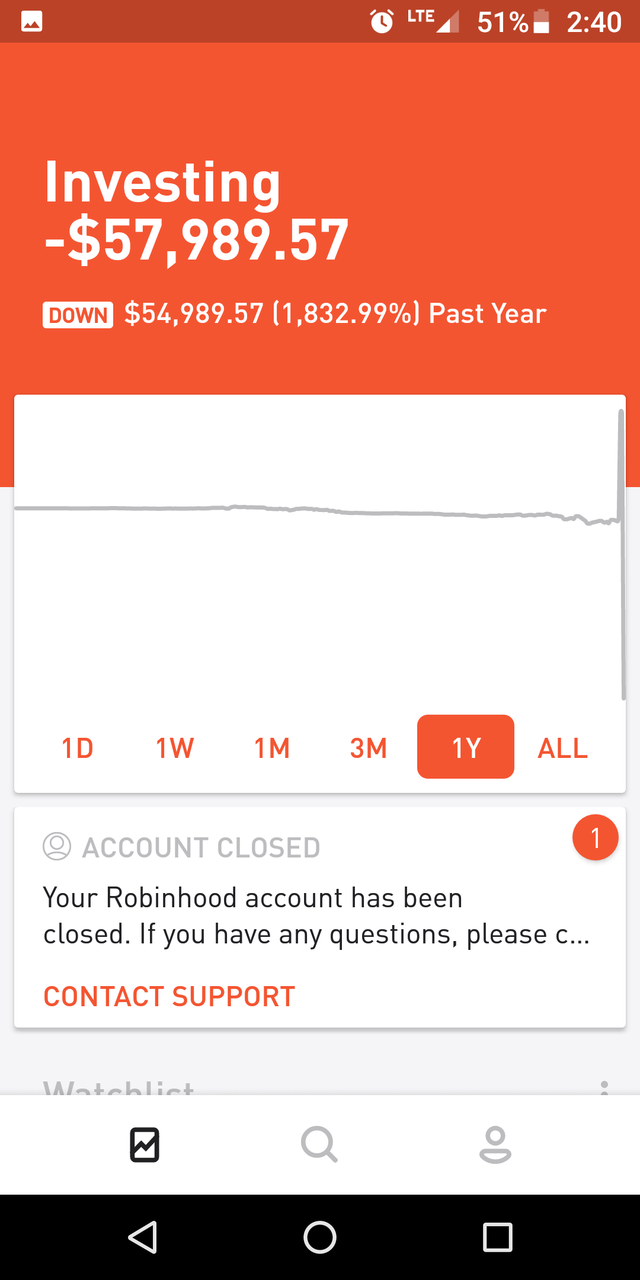

I wish I could say that this story was fictional, but to the best of my understanding this is more or less what /u/ControlTheNarrative and others attempted to do on Robinhood. Substitute "lemonade" for "AMD stock", and "lemonade coupon" for "deep-in-the-money covered call option". Theoretically, Robinhood shouldn't allow you to buy options on margin, but /u/ControlTheNarrative was very clever to use covered call options, which meant that he bought AMD stock with margin (valid) and then created cash and in-the-money AMD call options (sort of like creating matter and antimatter from nothing). Robinhood failed to detect the "antimatter", allowing /u/ControlTheNarrative to mask his "debt", thereby doubling his apparent net assets.

Ok, where did /u/ControlTheNarrative go wrong? It might be possible to still turn a profit by investing the vast amount of leverage in a “safe asset”, right? This seems unlikely: Robinhood’s interest rate of 5% far exceeds the risk-free rate of 1.88% currently offered by a 1-year Treasury note. In other words, it only makes sense to use Robinhood's leverage when you have the ability to deliver annualized returns that exceed 5%. When one has limited assets and a risky investment opportunity, they should instead carefully choose leverage so that they do not end up owing 10x their net worth should they encounter a stroke of bad luck.

Instead of trying to find an investment that minimizes risk while maintaining >5% return, /u/ControlTheNarrative proceeded to then take his enormous leverage and bet all of that on a coin toss: out-of-the-money (OTM) put options against Apple (remember that he is able to buy these options with leveraged cash because it has been "laundered" using covered call options).

Unfortunately for him, Apple proceeded to beat performance expectations for earnings, and subsequently the OTM options became worthless!

Guh!

Thanks to Ted Xiao and Daniel Ho for insightful discussion. We had a good laugh. I found the following links helpful in my research:

I wrote on Quora in Dec 2014 on why lowering the barrier to entry to this extent can cause retail investors to make trades without knowing what they are doing. That post turned out to be rather prescient, for reasons I’ll explain below.

One of the ways Robinhood makes money is via margin lending: they loan you some extra money to invest in the stock market with, and later you pay back the loan with some interest (currently about 5%).

If you are in the business of lending money, not only do you have to safeguard your brokerage system against technological vulnerabilities (e.g. C++ memory leaks that expose users’ trades), but you also need to defend against financial vulnerabilities, which are portfolios that expose the lender or its customers to an irresponsible amount of investment risk.

In the last few months it has come to light [1, 2, 3, 4, 5] that there are some serious financial vulnerabilities in Robinhood’s margin lending platform, whereby it is possible for users to borrow much, much more money from Robinhood than they are supposed to.

These users subsequently gamble huge amounts of borrowed money away in a coin toss, leaving Robinhood in a very bad spot, perhaps even at odds with Regulation T laws (I am not a lawyer, just speculating here).

“Leverage” is one of the most important concepts to understand in finance, and when used judiciously, is a net positive for everyone involved. It is important for everyone to understand how credit works, and how much leverage is too much. Borrowing more money than you can afford to pay back can take many forms, whether it is taking on college debt, credit card debt, or raising VC money.

Here’s a tutorial on “financial leverage” in the form of a story about lemonade:

Lemonade Leverage

It’s a hot summer, and you decide to start a lemonade stand to make some money. You have 100€, with which you can buy enough ingredients to make 120€ of lemonade for the summer. Your “return on investment”, or ROI, for the summer is 20%, since you ended up with 20% more money than you started with.

You also figure that if you had another 200€, enough people want lemonade that you could sell three times as much lemonade and make 360€. But you don’t have 200€ to spare! What do you do?

You could use the 120€ to build a slightly bigger lemonade operation next year. Assuming you could get a 20% ROI again next summer, you end up with 144€. But it will be many years before you even have 300€! By this time next year, lemonade might be out of fashion and kids might be juuling at home watching Netflix instead. You would much prefer to scale up your lemonade operation now, while you are confident that you can sell lemonade at a "profit margin" of 20%.

Fortunately, your friend “Britney Banker” is very wealthy and can lend you 200€. Britney Banker doesn’t have your entrepreneurial spirit, so she lacks the ability to get a 20% ROI on her own money. She offers to give you 200€ today, in exchange for you giving her 210€ at the end of the year -- an interest rate of 5%. Your “capital leverage ratio” is 100 / 200 = 1:2, because for every dollar you own, Britney is willing to lend you 2€.

If things turn out well, you sell 360€ worth of lemonade, pay Britney back 210€, and pocket the remaining 150€. Starting with 100€, you were able to use borrowed money to “magnify” your return to 50%.

However, if you make 200€ worth of lemonade and fail to sell any of it before the lemonade spoils and became worthless, you would be in a very sticky situation! You would have worthless lemonade and a 210€ debt to Britney. This is far worse than if you had lost your own 100€, because at least you wouldn’t owe anyone anything afterwards. So even though 1:2 leverage may amplify your gains from 20% → 50%, so it may amplify your potential losses from 100% → -310%!

The only reason why Britney is willing to lend you the money in the first place is that Britney thinks this outcome (you losing all of the borrowed money on top of your own assets) is unlikely. If Britney thought that you were less reliable, she might offer you a smaller leverage ratio (e.g. 1 : 1.5).

Lemonade Coupons

Suppose you make a big batch of lemonade (with Britney’s money) and then go door to door selling lemonade, but instead of giving customers a delicious drink right away, you give them a “deep-in-the-lemonade covered call option”. You take their money up front, and give them a coupon that allows them to “buy” a lemonade for free (0€).

The "call option" is referred to as "covered" because you actually have the lemonade to go with the coupon, it's just that you're holding onto the lemonade until the buyer actually redeems the coupon.

You then go back to Britney and say “I have 360€ of lemonade that I’ve made but haven’t sold, and 360€ in cash from selling lemonade options to customers, and as for debts there’s 200€ I’ve borrowed from you. That’s 520€ in net assets, so can I please borrow 1040€?”.

Britney says “sure, that’s a 1:2 leverage ratio”, and writes you a check for 1040€, again with 5% interest. But Britney has made a tragic mistake here! The 360€ in lemonade she counted as your assets are not really yours to spend, because you actually owe them in obligations to customers.

With 1204€ in borrowed assets, you are now leveraged over 1:12 !

You repeat this process again, turning 1040€ cash into 1248€ of lemonade, selling an additional 1248€ of deep-in-the-lemonade options. You now have 1608€ of lemonade, and 1608€ in cash, and 1204€ of debt, for net assets of 1608 + 1608 - 1204 = 2012€.

You go back to Britney and ask to borrow another 4024€, with 5% interest. Again, because Britney is forgetting to account for the 1608€ in lemonade “debt” that you may have to deliver to coupon-holders, she thinks that the leverage is still 1:2. You repeat this process one more time, and your new total position is 6k€ in lemonade, 6k€ in cash, 5k€ net debt.

If you were to successfully deliver 6k€ of lemonade, you would make 1k€ in profit, starting from only 100€ of your own cash. A 1000% return sounds too good to be true, right? That’s because it is.

One hot summer day, all of the coupon holders decide to exercise their coupons at the same time. You realize that your lemonade stand can’t actually fulfill 6k€ in lemonade orders and you are in way over your head. Desperate, you attempt to pivot and come up with a Billy Mcfarland-esque scheme to buy lemonade from a local grocery and dilute it with some water. But due to inexperience with food handling operations, you accidentally contaminate half the batch, and are left with only 3k€ of lemonade. You have 6k€ cash but still owe 3k€ in lemonade and 5k€ in cash.Your 1k€ profit opportunity has now become a 2k€ DEBT (ROI of -2100%), and we haven't even factored in the interest! Because the debtors (lemonade coupon holders and Britney Banker) must be paid regardless of whether you successfully make lemonade or not, your leverage has an asymmetric payoff - the downsides are twice as bad as the upside!

I wish I could say that this story was fictional, but to the best of my understanding this is more or less what /u/ControlTheNarrative and others attempted to do on Robinhood. Substitute "lemonade" for "AMD stock", and "lemonade coupon" for "deep-in-the-money covered call option". Theoretically, Robinhood shouldn't allow you to buy options on margin, but /u/ControlTheNarrative was very clever to use covered call options, which meant that he bought AMD stock with margin (valid) and then created cash and in-the-money AMD call options (sort of like creating matter and antimatter from nothing). Robinhood failed to detect the "antimatter", allowing /u/ControlTheNarrative to mask his "debt", thereby doubling his apparent net assets.

Ok, where did /u/ControlTheNarrative go wrong? It might be possible to still turn a profit by investing the vast amount of leverage in a “safe asset”, right? This seems unlikely: Robinhood’s interest rate of 5% far exceeds the risk-free rate of 1.88% currently offered by a 1-year Treasury note. In other words, it only makes sense to use Robinhood's leverage when you have the ability to deliver annualized returns that exceed 5%. When one has limited assets and a risky investment opportunity, they should instead carefully choose leverage so that they do not end up owing 10x their net worth should they encounter a stroke of bad luck.

Instead of trying to find an investment that minimizes risk while maintaining >5% return, /u/ControlTheNarrative proceeded to then take his enormous leverage and bet all of that on a coin toss: out-of-the-money (OTM) put options against Apple (remember that he is able to buy these options with leveraged cash because it has been "laundered" using covered call options).

Unfortunately for him, Apple proceeded to beat performance expectations for earnings, and subsequently the OTM options became worthless!

Guh!

Acknowledgements

Thanks to Ted Xiao and Daniel Ho for insightful discussion. We had a good laugh. I found the following links helpful in my research:

- https://www.reddit.com/r/wallstreetbets/comments/dqg6xx/infinite_leverage_explained/

- https://www.bloomberg.com/opinion/articles/2019-11-05/playing-the-game-of-infinite-leverage

No comments:

Post a Comment

Comments will be reviewed by administrator (to filter for spam and irrelevant content).